At the risk of not listening to our wonderful founding father, Allen Jacobson, who advises to always accentuate the positive, this might come off as a negative piece.

I’m just going to state that now, so it’s out of the way. Our goal here is really to help make GOOD decisions, which should lead to better outcomes. Better outcomes are POSITIVE!

But in the spirit of one of the smartest people of the past 100 years, and one of the best investors of that time, Charlie Munger, who said “invert, always invert”, we’re going to use that technique here, and if it gets you to think…mission accomplished. Our list below isn’t exhaustive by any means, but it’s a start.

So now, let’s invert and ask what seems like a silly question:

How Can I Get Lousy Investment Results?

FORGET THE FUTURE. Investing, by its nature, is always about the future. Think about it – to invest, one chooses NOT to spend but instead to save, and then invest in something for some day that’s in the future. So, our first way to get poor investment results is to cling to the past – don’t invest for the future, but invest because you’re trying to rectify some wrong, or fix something in the present. That’s likely not going to do what you were hoping.

Investing is not about the past. Or the present. Investing is always for the future. Never, ever forget that.

HAVE NO PURPOSE. Next, once we decide that we are going to invest, for the future…we must connect our investments to that future. Who are you investing for? What cause? What purpose? Those decisions are going to build the foundation for how you should build your portfolio.

We say, “Give Your Money a Mission”. Mission, purpose….same concept. What is yours?

Most huge investing mistakes are made when we forget what our purpose is, even if momentarily. Don’t forget yours.

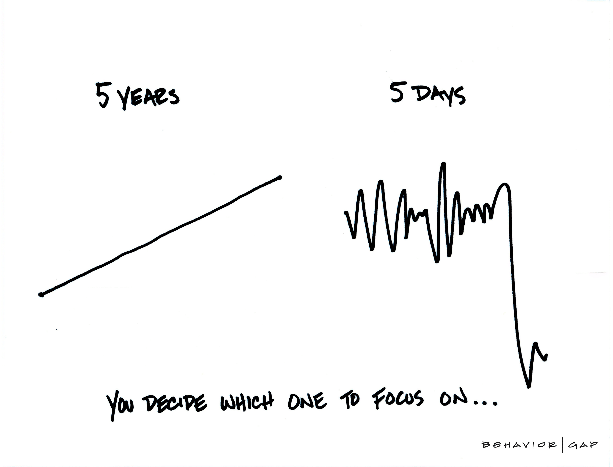

CHECK YOUR BALANCES FREQUENTLY. Watching investments fluctuate in value does little good. Mostly, it messes with our minds, because, if we’re growing our portfolios, higher dollar amounts translate to higher daily or weekly paper losses. 2% on $1,000 is 20 bucks. But 2% on $1,000,000 is $20,000. Yet, a 2% move with investments is quite common. Without perspective, context, or maybe even “brain training”, that can come with all kinds of feelings that aren’t helpful for sticking to our plans or investing both for the future and for our purpose. It can often lead to…

PANIC. We all get emotional. It’s in our DNA. In fact, us mere humans are wired to rely on emotions to help us make better decisions and, in extreme cases, this can be instrumental in saving our lives

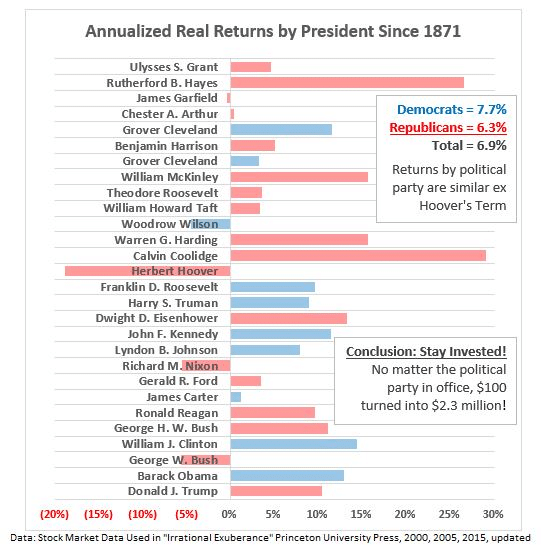

INVEST ACCORDING TO YOUR POLITICS. It’s fine to have views on politics. But don’t give politicians more credit than they deserve. They change constantly. They’re trying to stay in power…after all, isn’t that “the game”? They don’t run companies, though.

And politics have nearly always been nasty. Remember, a sitting U.S. vice president once shot and killed a former treasury secretary in a duel! When you’re rational, just realize that it hasn’t

A political wind isn’t usually going to mess with that too much, or for very long. Don’t let your political views influence your investing, because…markets don’t care about your politics. You do. It’s a trap. Barry Ritholtz said it well in the Washington Post.

READ TOO MUCH NEWS. The internet has flattened barriers to creating headlines. Nowadays, almost anyone can “be a writer”, and that means: 1) There’s more content to read and 2) The quality of content has worsened. Plus, a side effect has emerged online wherein context, nuance, and “gray areas” seem to have disappeared, all because headlines are after “clicks” and tend to be hyperbolic and/or polarizing. But, the world’s truly greyer than “black and white”. Shane Parrish over at Farnam Street has said this better. What’s worse is that bad news sells, while good news doesn’t. Reading the headlines risks convincing us the world is terrible. Yet, in another view, the world keeps getting better. The news is just messing with our minds, making it hard to make good decisions.

Consider much of the news as “junk food for the brain”.

“Follow the trendlines, not the headlines!” – Bill Clinton

“…Humankind is advancing, however haltingly and imperfectly, toward a better world” – Steven Pressfield, The War of Art

“Should you ever listen to pessimists? Of course. They’re the best indication of what’s unsustainable, and thus probably about to change, and thus probably the soil of what’s to be optimistic about. -Morgan Housel, Motley Fool”

“There are few wealthy pessimists” – Jack Butcher

TRADE FREQUENTLY. Years ago, a study by Fidelity made some rounds, wherein they found that investors who forgot they had an account did better than those that logged in frequently. They’ve also found that women, on average, trade less than men and get better investment performance. Many academic studies confirm that higher “turnover” portfolios (turnover is a term for selling & buying) typically do worse – perhaps the best of which is buried in a 2016 working paper from Martijn Cremers at Notre Dame (this one’s really technical). Trade when necessary. Not more.

TRY TO TIME THE MARKETS. It’s a superpower we all want, but superheroes aren’t real. Nobody can do it. Not you. Not Warren Buffet. If you could, you’d eventually have all the money in the world (we actually researched this topic and proved that to be true). Maybe you get it right once, or twice. You’ll have to get lucky, because just a few days each year typically matter tremendously – see #3 here). So even if you get lucky, odds are you can’t repeat that. More likely you’ll overtrade as you gain “confidence” and wind up as a statistic in Fidelity’s study of poor performers.

HOLD A PORTFOLIO JUNKDRAWER. We’ve looked at hundreds of outside portfolios over the years. The one that perhaps frustrates us the most is one where there are just too many mutual funds (more than 5-8, really, but we’ve seen over 50 in a single investor’s portfolio). We can’t figure out a purpose to investing this way, other than, probably, to generate fees for someone else (not the investor). This looks like a “junkdrawer” to us – a collection of stuff, without much direction or reason, and it’s not likely to get good results.

WORSE YET – MAKE THAT “ALL THAT STUFF” EXPENSIVE. Even more, we frequently see those junk drawers with 2-3% total annual fees, often unbeknownst to the investor. That’s going to act as a very heavy anchor on a portfolio, and is super likely to generate 2-3% worse results every year than intended (our experience tells us it typically winds up even worse than that, if you can believe it). And that will add up to be lost dollar amounts that are so big that most people can’t comprehend, because of compounding.

“Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t pays it.” – Attributed to Albert Einstein but there’s no actual evidence it was him

LOAD UP ON DIVIDEND STOCKS AND JUNK BONDS, BUT PAY NO ATTENTION TO THE BUSINESSES TO WHICH THEY ARE ATTACHED. We see this one a lot, also. We’re not against dividends, junk bonds, private investments, or any specific “income generating” asset, in general. But we do see too much emphasis on these types of holdings, without much discussion about their downsides. Junk bonds often show high income potential, but make no mistake, they’re a very volatile asset class – they move up and down almost as much as stocks, yet don’t have anywhere near the upside. Understand them.

The same goes with dividend payers. Too often, a high-dividend-paying stock is a company that’s not particularly competitive or being mismanaged. GE, Wells Fargo, CenturyLink….there are many stories of companies that looked like “solid, blue chip, income holdings” which have gone on to fail to deliver that need. An uncompetitive or poorly run company is to be avoided….no matter the dividend.

IGNORE TAX EFFICIENCY. Let’s start by saying that we aren’t against paying taxes. However, we do think there can be weird tax things that investors often do that hurts their results. This is a complicated topic that can take many different directions, but the point is, don’t ignore tax efficiency – and that means BOTH in the short-run (say, this year & next), but ALSO the long-run (your lifetime)!

USE OPTIONS. Options are a fun way to gamble in markets. But here’s the thing…while it’s hard enough to figure out if a company’s stock is going to be a good investment….options make it more difficult by adding an element of trying to “guess” both a future price AND at a specific time. And time often works against you. Why make an already difficult decision even harder? To be fair, options have value, but they are a complicated instrument, and should only be used by investors that really understand them, and even then, probably not with your life savings.

FALL FOR THE ‘TOO GOOD TO BE TRUE’ INVESTMENT (OR COMPLEXITY). We all want it….that elusive investment that only goes up, never goes down, and generates incredible annual returns. It looks like this red line below (“Fairfield Sentry”) over time.

Don’t fall for it….the red line was Bernie Madoff’s flagship fund’s purported performance history. But as we all know, it was…well…you know. You aren’t likely to find good returns without risk. If you think you’ve found a way…dig deeper…because there’s a good chance you’re probably missing something. Take this next example – where some pension funds lost money with a complicated hedge fund that didn’t live up to its promise (few hedge funds live up to their promise, by the way).

Good investing starts with a purpose in mind. As that purpose shifts around with life, it’s very appropriate to make changes accordingly. But, if you find yourself doing these things we’ve listed, you’ll likely get bad results. That will cost YOU, YOUR FAMILY, or YOUR CAUSES. It will be deserved (sorry).

But….here’s the good news, and where we come back to the positive and follow Al’s advice. These things are all choices, and controllable. You don’t have to do ANY of them! In fact, if you don’t, you’re likely on a path that’s headed towards a good outcome. So, when times get emotional and you think it’s time to deviate, practice mindfulness…take a breath and ask, “should I really do this, based on my purpose?”