As people consider retirement, here’s a question we get A LOT (the question has many variations):

Question: I need income during retirement, so does that mean you will emphasize dividend-paying stocks?

Our answer often surprises people: NO. We don’t find that to be efficient.

We get it. People want to live off their portfolios, and it’s easy to see the allure of owning companies that make generous cash payments to investors. When you think about it, it makes a whole bunch of sense.

However, our preference is to focus on “Cash Flows” and not dividends or “income.”

Our view is that money is money, no matter where it comes from. Any form of cash flow can be spent.

Perhaps that sounds fine in theory, but let’s discuss an example.

This case study is a real-life example, with actual data from an “income portfolio,” though it’s been anonymized, and dollar amounts have been scaled. We also removed fees here, which we’ll cover in the next piece (so we’re really just showing theoretical values, but we have the real data, and what’s below is directionally accurate.)

Here are the goals this investor had:

Investment: $500,000

Goal: Withdraw $22,500 per year ($1,875 per month as “paycheck”)

Withdrawal Rate: 4.5% per year

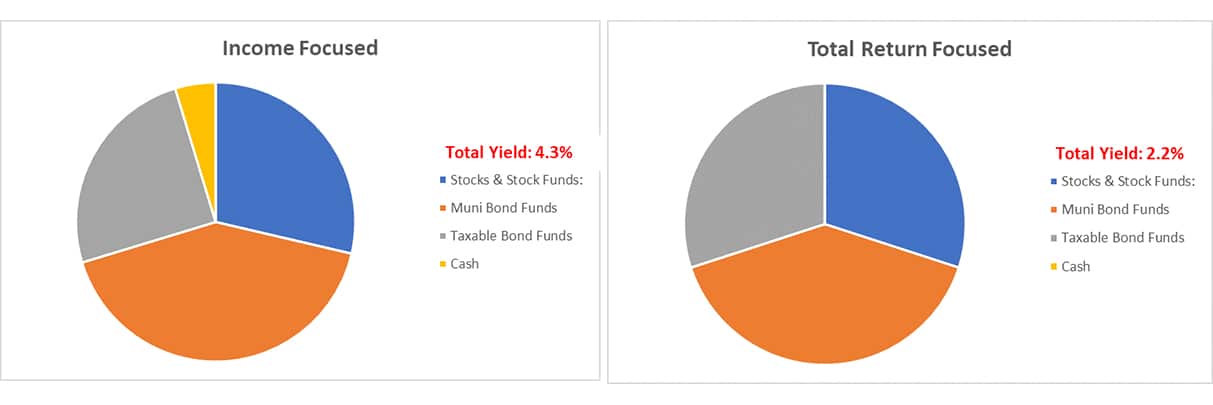

As investors, we think the word “return” is a very important one, so humor us here. We’ve named one portfolio the “Total Return Focused” portfolio (below, on the right). We’re going to compare that to the income-focused portfolio of our investor in the case study. The portfolios are constructed similarly, with a small exception of some cash (not really an important detail). The key highlight here is in RED.

The Income-Focused portfolio contains high-dividend stocks, high-dividend stock funds, and high-yield bond funds, producing a 4.3% yield. In other words, it becomes easy to see how that portfolio should be able to generate the $1,875 per month because it’s expected to generate $1,792 per month of “income” due to dividends and interest from the bonds. At least, that’s how it starts.

The portfolio on the right, our Total-Return portfolio, doesn’t look like it will work out well, with just a 2.2% yield, or $917 per month. That seems like less than half of the income that’s needed to support the goal.

The Income-Focused portfolio looks like the clear winner—with nearly twice the income of the other portfolio, despite having a similar allocation to stocks and bonds. Which one would YOU choose?

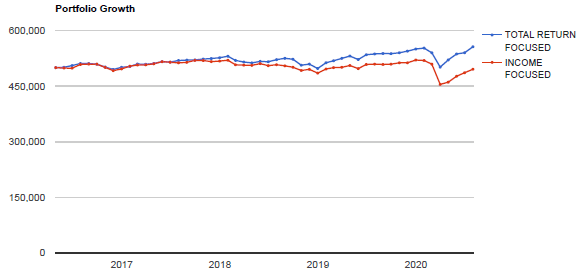

Now let’s fast forward – what actually happened over the next four years? (May 2016 to July 2020). Using Portfolio Visualizer, we were able to load the results (not counting fees, which we’ll cover later).

Answer: The income portfolio has done its job – after withdrawing the monthly “paycheck” of $1,875, its final value is still about the same as the starting principal of $500k. SUCCESS!

But wait a minute. The total return portfolio has more money in it? How can that be, you ask? The details behind the how, what, and why will follow in our next piece (and you’ll see that actual results of this “income portfolio” were not as good as shown here).

For today, here’s our main point: JSA FAVORS THE TOTAL-RETURN STYLE OF INVESTING. When it comes down to styles of investing, we won’t focus on “yield,” “income,” or dividends as our key decision point. We’re actually going to go well beyond that.

The income portfolio above, by many measures, would be considered successful. However, we prefer clients to make more money over time, AND earn adequate retirement income. To us, this is better investing because of increased flexibility, improved tax efficiency, better inflation protection, and added value over time.

Follow up #1: A deeper dive into actual results (and why they were worse)

Follow up #2: What is a dividend, where does it come from, and how does JSA consider them?

Jacobson & Schmitt Advisors, LLC (“JSA”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where JSA and its representatives are properly licensed or exempt from licensure. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security.